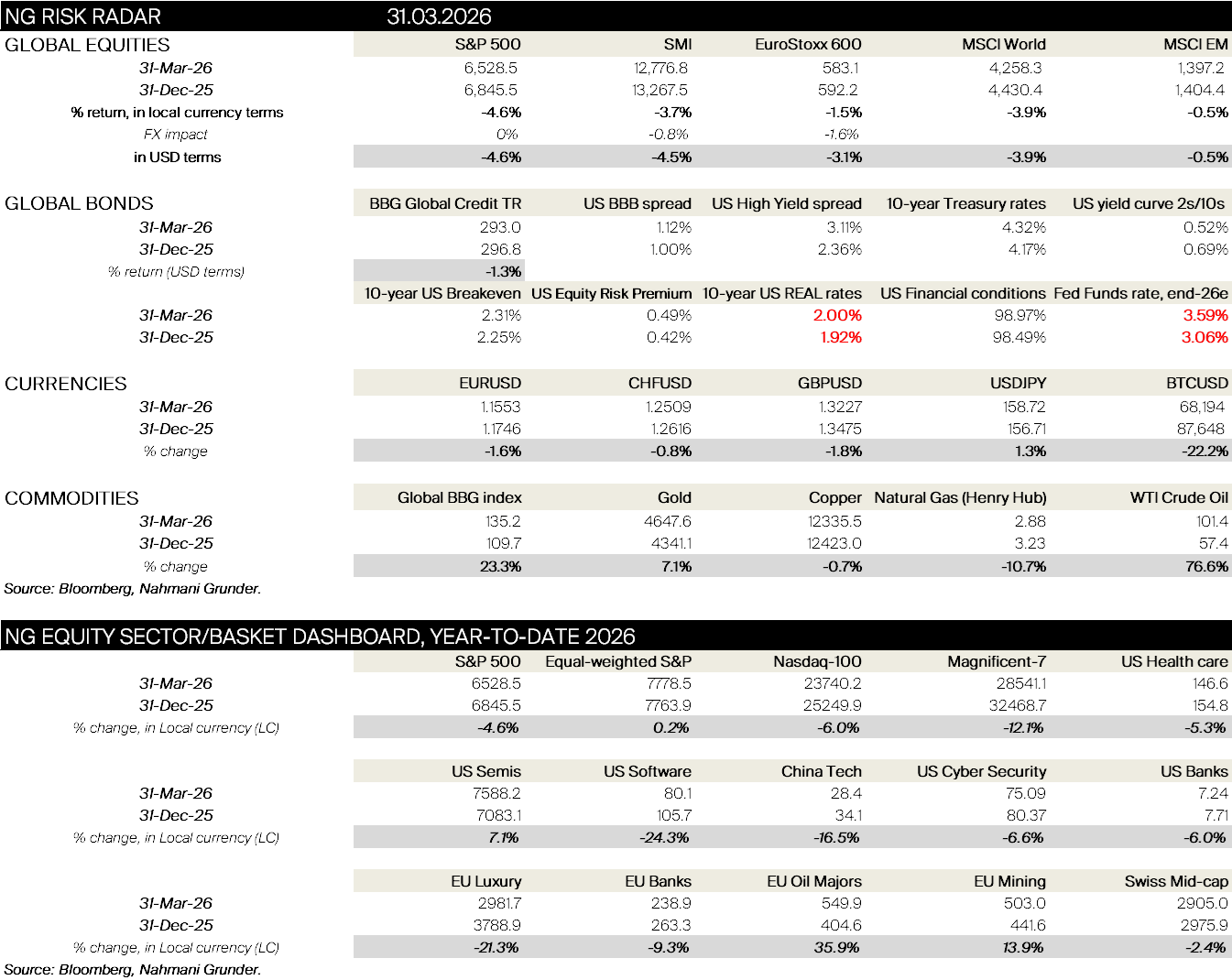

March witnessed significant volatility across global markets, characterized by the sharpest monthly declines in years.

Stoxx 600 recording its biggest monthly drop since 2022 and its second biggest since the covid pandemic in March 2020 (SXXP -8%). S&P down for the 3rd time in the past four months (-5%) and NDX (-5%) having its worst month since March 2025. The sell-off was broad-based with S&P equal weight down -6%. Markets reversing sharply lower from the 28th February when US and Israel targeted Iran and killing of its supreme leader. Subsequent closure of Strait of Hormuz and hit to Iran’s South Pars and Qatar Ras Laffan facilities wiped out 17% of global LNG capacity.

European natural gas prices hit its highest level since Jan 2023 at €74/Mwh and Brent prices soared +43% spiking at $120/bbl before now settling around $100/bbl. Worries around inflation led to significant repricing of rates with the US 10yr briefly touching levels we haven’t seen since Summer 2025 at 4.4%. Gold gave back much of its outperformance in February and was down -11% for the month (+7% YTD). Market started to reprice central banks hikes and now have 3 priced in for the ECB by Year-end, FED still priced to cut by 25bps with a 35% of a chance of a hike at this point.

However, fundamentals are still more than decent, reinforcing the view that weakness should be temporary as the medium-term backdrop is more constructive: US earnings remain resilient, balance sheets are solid and history suggest that geopolitical shocks are often a good buying opportunity but as discussed, this morning not much for us to do here.