1. Geopolitics

Focus will continue to be on the Middle East and Iran for the foreseeable future. Key questions are the extent of escalation, the length of conflict and the knock‑on effects. Around 20% of the world’s oil passes through the Strait of Hormuz, which is only 33km wide at its tightest point, and 15% of the world’s aluminium is produced in the region. Oil accounts for roughly 20% of China’s energy needs, with a meaningful share coming from Iran. The GCC has criticised Iran’s decision to attack Gulf states; a senior policy adviser to the UAE president said: “Your war is not with your neighbours, and through this escalation, you confirm the narrative of those who see Iran as the region’s primary source of danger.” The succession question around Ali Khamenei, and whether we are on the precipice of regime change, will shape the outlook for the Iranian regime in the short, medium and long term. All of this will feed through to global markets, risk premia, oil and natural gas, inflation, global trade and overall risk sentiment. This also matters for the upcoming Xi Jinping–Trump summit in China in about a month, where the backdrop to US–China relations will be very different.

2. Politics

Trump was elected on an America First mandate, and the Venezuelan and Iranian interventions risk unsettling parts of his base. How the public reacts to his decision to act on Iran will be important as we approach the midterms.

3. AI capex and ROI on capex

The headline AI capex numbers have escalated quickly: 150bn dollars became 300bn, then 500bn, and are now expected to reach the 600–800bn range in the coming years. The current quarterly capex run rate for Amazon, Alphabet, Microsoft, Oracle and Meta is around 130bn dollars, roughly three times what it was only two years ago. The natural next question is what level of revenue is required to pay back and generate an appropriate return on this capex, and when that revenue will actually flow through. These companies have shifted from cash‑printing machines with oligopolistic positions in their verticals to cash‑spending machines engaged in a “no choice but invest” AI arms race. As in past capex booms (rail, telecoms, internet), who the winners and losers are will only be clear in the future, and the timing of “winning” will vary. We have already discussed this, but one key point to watch is that the 667bn dollars of hyperscaler capex expected in 2026 would consume over 90% of operating cash flow, only risk to this is if one’s growth does slow down.

4. Flight to safety

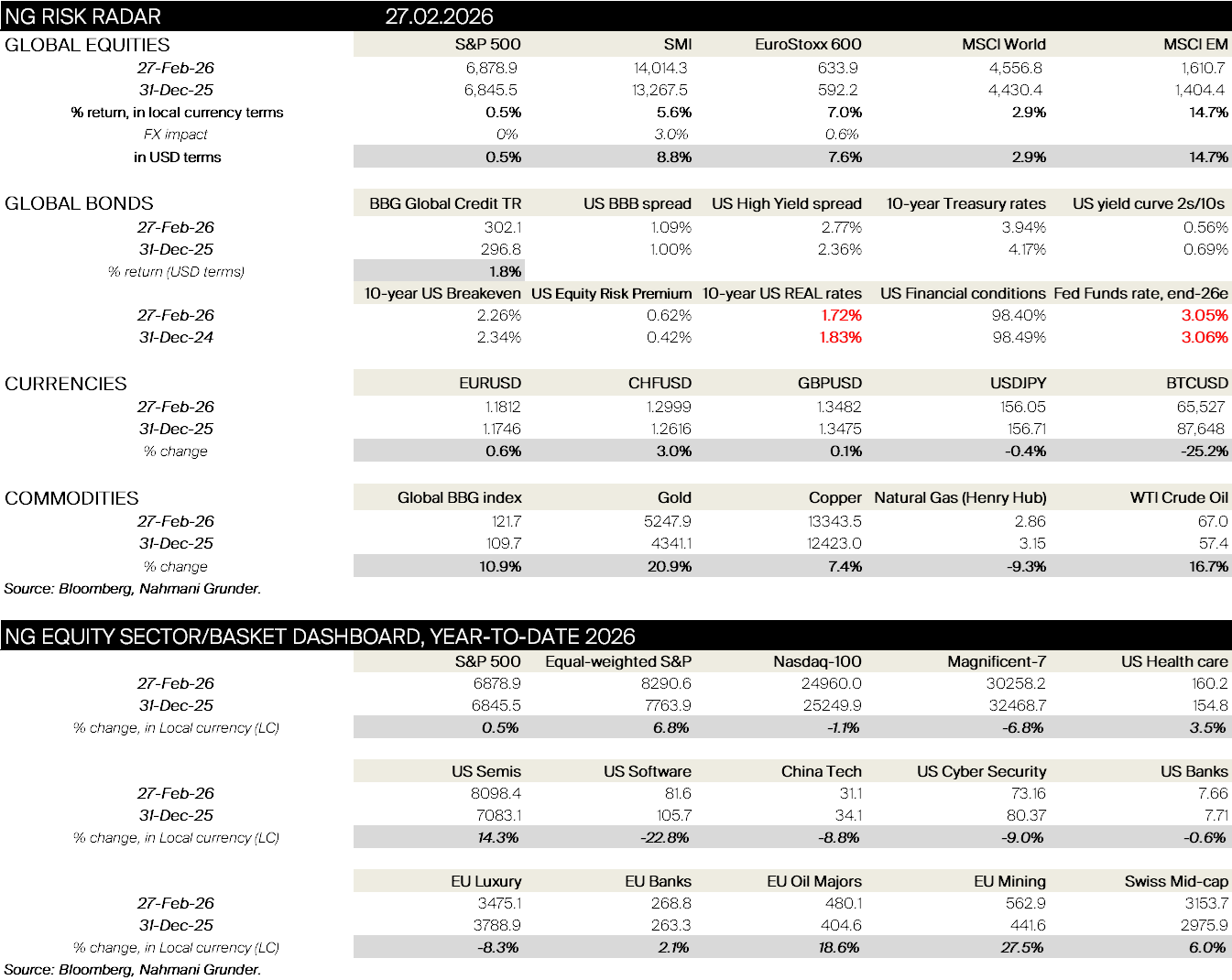

The dollar has rallied hard since the Iran attack. Gold (BTC remains unloved) is back within touching distance of all‑time highs. In the near term, the “usual” reaction pattern remains in place: gold up, oil up, volatility up and rotation into defensive proxies and safe havens, on that point the Swiss National bank today announced that it is carefully watching strength in the CHF.

5. Broadening and diversification

Regional performance is a reminder that there is a game outside the US. Korea is up around 40%, Taiwan 25%, Japan 17%, the UK 10% and Europe 7%, compared with the S&P up about 50bps, the Dow Jones up 1.9% and the Nasdaq down 1.1%. Being overly invested to the US and US businesses has paid handsomely over the last decade and whilst we have seen this trend before I wouldn’t be chasing to make greater investments elsewhere given the disconnect with valuations (Semis and Memory players in Korea for example).

6. Volatility

It is hard to reconcile how a market with this much going on had the VIX with a 19 handle last week. Today its spiked 18%, but beneath the surface the statistics point to elevated volatility at the single‑stock and theme level versus almost at any point in history. Similar to index performance this year, the headline index number understates the amount of dispersion and cross‑sectional risk that is actually being repriced.