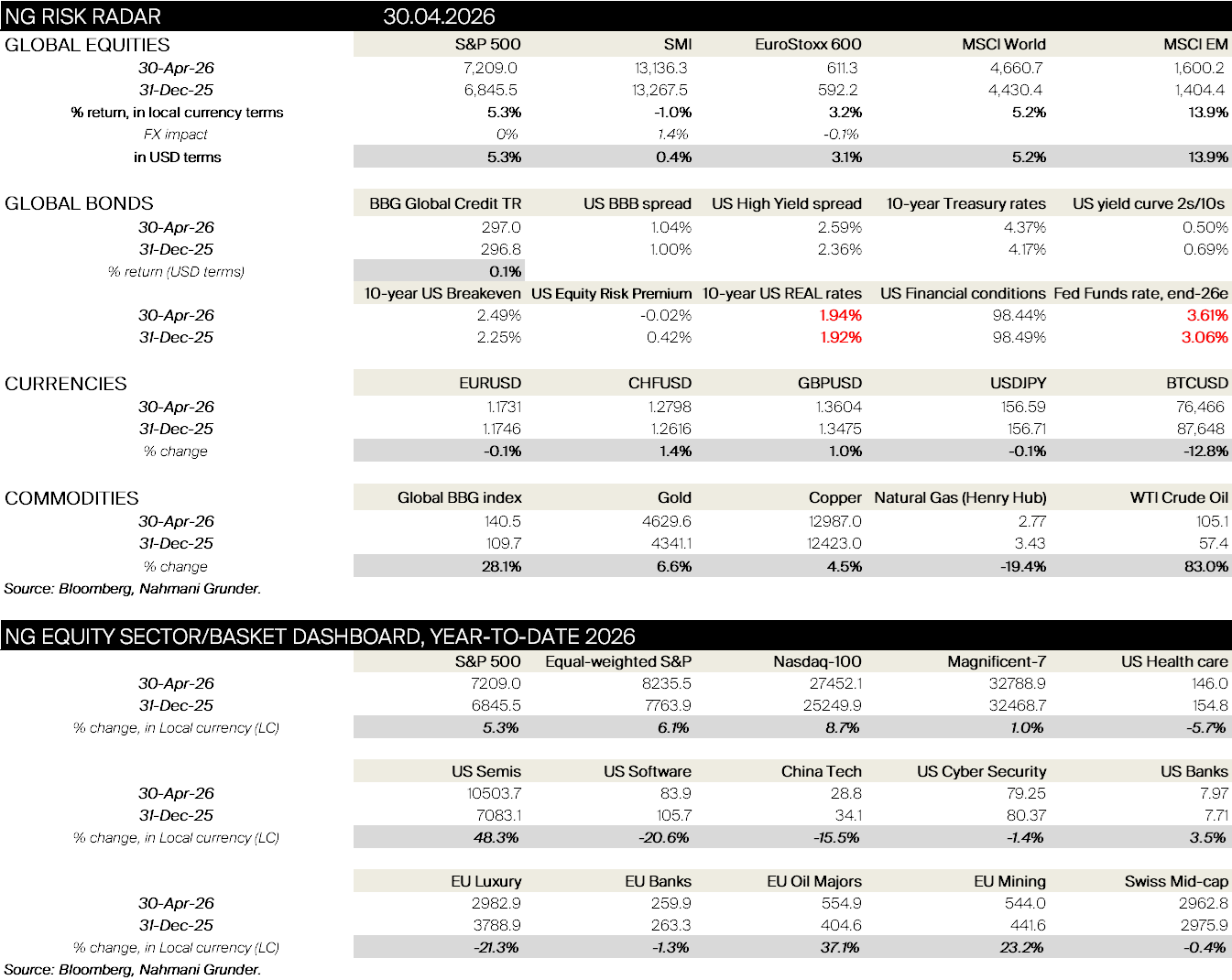

Equities traded sharply higher in the month of April with S&P (+10%) and NDX (+15%) posting new ATHs and having its best returns since 2020. Europe with SXXP +5% as we saw 10yr German Bund yields rising to 3.1% which is levels we haven’t seen since 2011 and UK 10-year Gilts reaching 5.1%.

War in Iran continued to be front and centre where April started with a potential offramp optimism as Trump signalled willingness to wind down his military campaign. Though mid-month the US announced its own blockade of the Strait of Hormuz to get Iran back to the negotiation table. Negotiations however stalled and Trump rejected Tehran latest offer while reports said US may be considering more strikes to break the stalemate. Monetary policy expectations swung sharply where markets at peak tension priced multiple hikes from ECB as early as April but as energy prices retraced this was aggressively pared back. By month-end ECB and BOE signalled caution and data dependence.

In the US we’ve seen the economy holding strong with NFP rebounding +60k from the -92k decline in February, initial claims falling to 189k which is lowest since 1969. In Europe we’ve seen weakening momentum with Sentiment indicators deteriorating (IFO, consumer confidence) while April flash PMI’s moved to contraction territory for the first time in over a year. Brent reaching $126/bbl after 8 straight days of gains which is levels we haven’t seen since Russia’s invasion of Ukraine. Oil prices have however given back some of these gains in the last two days and is currently trading at $105/bbl. In the last week UAE also announced that they will leave OPEC which will more than likely impact oil prices longer-term. Gold is once again doing the job it should be doing.

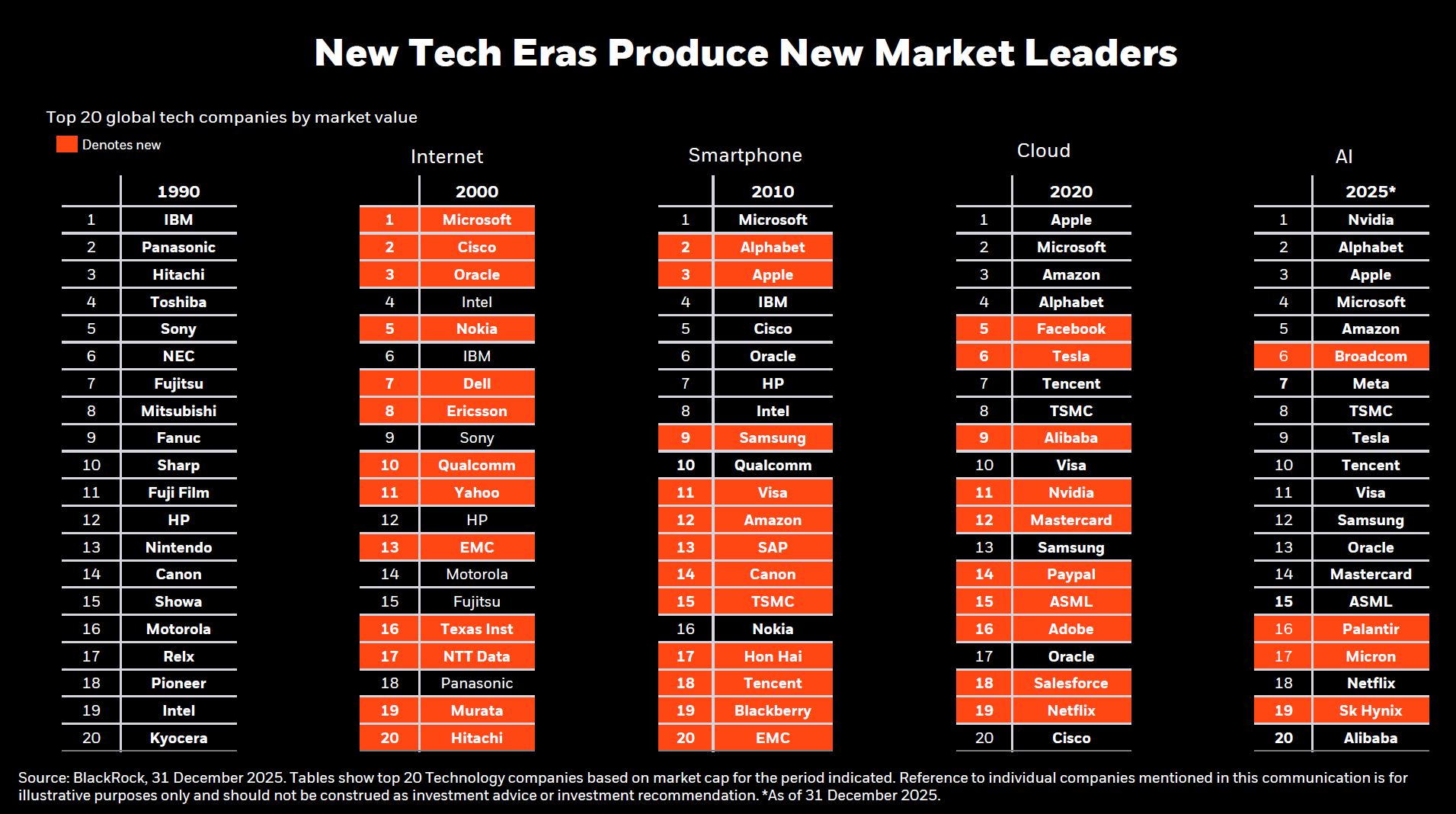

Fewer stocks are driving the strong performance especially in the US where market breadth is deteriorating as Google +34%, AMZN +27%, Broadcom +33%, TSMC +20% for the month. Semis hit a record 18th day winning streak before news of a report from WSJ saying OpenAI missed several key internal growth metrics, which had investors questioning AI spending. Earnings continue to be strong, especially in the US, where the Hyperscalers capex now are projected to reach $700bn in 2026. Something though to remember from the past on breadth, while narrow breadth can resolve via either "catch up" or "catch down," both outcomes are characterized by the underperformance of previous market leaders.