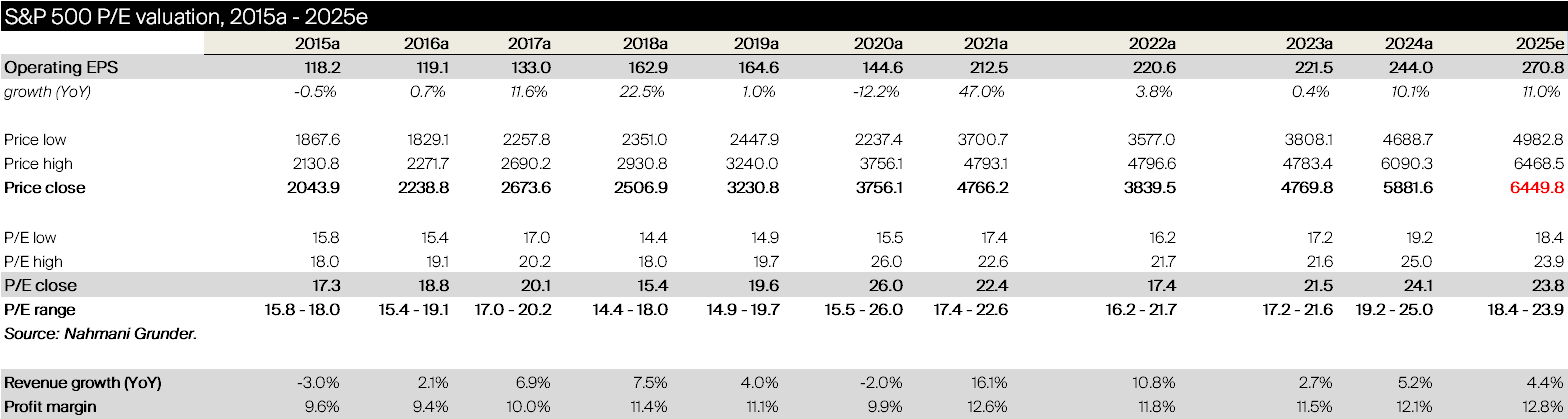

The US earnings season is well advanced with 90% of the companies having reported Q2 results by 8 August, with 81% of the S&P 500 constituents delivering a beat.

Similar to Q1, Q2 earnings collectively are thus way better than expected, with EPS growth at +11.8% YoY, versus NG forecast of +9.0% and consensus at +5% by 30 June. The upside surprise is mainly driven by Technology and Health care. This will be the 3rd consecutive quarter of double-digit year-on-year growth.

Q2 revenue growth is also better at +6.3% YoY, versus NG forecast at +4.0%, with net margin coming in at 12.8% so far.

Based on Q2 results, we are increasing our S&P 500 EPS forecast for 2025 from $ 268.8 to $ 270.8 (versus consensus at $ 267.5), implying EPS growth of +11.0% YoY (versus +10.2% previously).

The S&P 500 is now up +9.7% for YTD 2025 and is close to an all-time high with P/E 2025e of 23.8x. We believe S&P 500 should deliver another year of double-digit EPS growth in 2026 based on the proliferation of agentic AI solutions in the enterprise which would reduce the P/E to 21x for 2026. US equity markets are already partially pricing in an acceleration of EPS growth and further margin leverage from here unleashed by AI.

Our year-end 2025 price target remains 6,600. Our latest NG Market Insights is attached to this email.